Start transacting with us Register Now

Start transacting with us Register Now

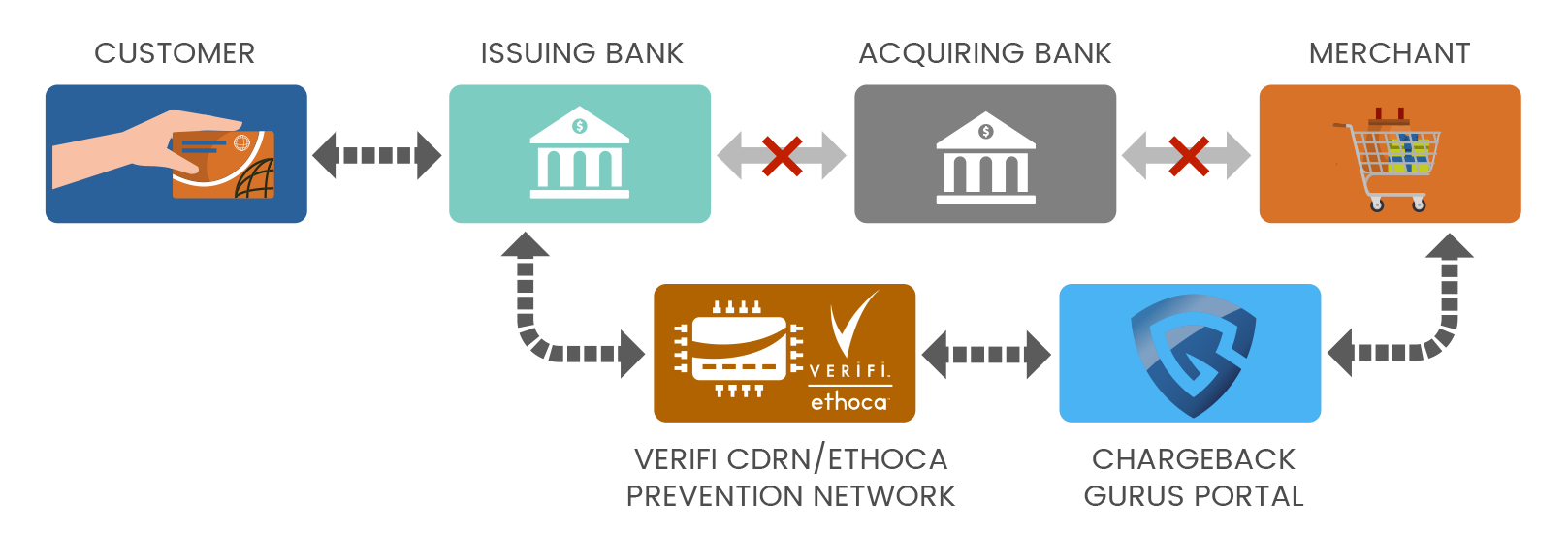

In simple words, Chargeback is a dispute against a particular transaction raised by the Cardholder (End-User), and reported to their Card Issuing Bank (End-User’s bank). It is a provision by Banks and Card Networks such as Visa & MasterCard to protect buyers from unauthorized or fraudulent payments. Once the cardholder files a complaint, the bank reports the same through the channels to AggrePay Payments Solutions Private Limited.

AggrePay then initiates an investigative procedure contacting the Merchant and in extreme cases the End-User.

There could be several reasons of Chargeback against a particular transaction. A list of the most common reasons of Chargeback is listed here.

Generally, Chargebacks can be associated with Unsatisfactory customer service/product or poor service delivery experience. Chargebacks can also be filed if the customer suspects fraudulent activity on their card.

It is best to avoid any kind of Chargeback, as banks and card networks can label your business as a fraudulent/high risk business, hampering your image. A customer has a timeframe of 120 days to file a Chargeback , which means your sales are reversible for that time period. A high number of Chargebacks can lead to the banks holding remittances for the business as well. The worst case scenario could be a ban of online payment services imposed upon the business.

Chargebacks should be considered High Priority issues due to the involvement of risk teams of both the customer’s bank as well as our partner banks. At AggrePay we have a dedicated team & process to resolve Disputes / Chargebacks. The following mentioned are the steps taken for a Merchant during a Chargeback. The customer has to go to their respective bank to file a Chargeback.

AggrePay will notify the Merchant by E-Mail about the dispute filed against them, mentioning the payment ID and the reason of Chargeback, if provided by the bank.

In order to represent the Chargeback - Review the Chargeback and explain to us the chain of events that took place.

In case the goods/services have not been provided - Review the issue and let us know if the customer is willing to accept the goods/services.

In case the goods/services have been delivered - Share the proof of deliveries, invoices, any other authorised proof of product/service delivery.

In case of a duplicate payment made - The Merchant should let us know so we can ask the bank to refund the amount back to the cardholder.

In any other cases - Share documents - Share all documents as per the requirement of the bank with us. We will represent the dispute on your behalf.

Banks generally provide a Window of 7 Working Days to represent the Chargeback. Failure to do so within the specified window will increase the number of Chargebacks lost by you. If you lose the chargeback, the amount will be debited from your settlement balance.

Emails with Proofs of Service / Delivery should be sent to compliance@aggrepay.in

As mentioned above, most of the Chargeback cases come up due to miscommunication between the buyer and the seller. Here are a few tips that you can keep in mind to avoid Chargebacks :

| Transparent Return Policy | Making sure the return policies are clearly mentioned on the website | |

|---|---|---|

| Constant & Clear Communication | Keep customers updated regarding the status of their order | |

| Proofs of Delivery | Share tracking numbers, invoices and all other order related docs and references with your customers | |